401(k) Retirement Calculator: Project Growth & Maximize Employer Match

To plan for long-term financial independence, you must understand how your current savings, ongoing contributions, and compound interest work together. A 401(k) retirement calculator estimates your future account balance by analyzing your current age, salary, personal contribution rate, employer matching limits, and anticipated market returns. By mapping these financial inputs, the tool projects your estimated retirement savings, calculates the monetary value of your employer’s match, and displays the upfront tax savings of pre-tax traditional 401(k) contributions.

To explore more conversion, financial, and metric calculations, visit our central /conversion/ hub.

The Mathematical Mechanics of 401(k) Growth

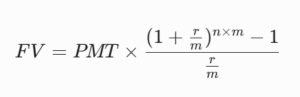

Unlike a standard savings account, a 401(k) portfolio grows through regular, automated contributions that compound over decades. The mathematical formula used to calculate the future value (FV) of periodic, end-of-period monthly contributions (PMT) compounding over time is:

Where:

- FV is the projected future value of your 401(k) balance.

- PMT is your total monthly contribution (including your personal pre-tax contribution and your employer’s matching contribution).

- r is the estimated annual rate of investment return (expressed as a decimal).

- m is the annual compounding frequency (typically 12 for monthly contributions).

- n is the total investment horizon in years (planned retirement age minus your current age).

How This 401(k) Calculator Evaluates Your Wealth

This calculator processes specific financial inputs to model your portfolio’s growth over time:

- Personal Inputs

- Current Age & Target Retirement Age: Determines your total accumulation phase (n). The longer your timeline, the more time compound interest has to accelerate your savings.

- Annual Salary & Contribution Percentage: Calculates your annual baseline contribution. For example, a 6% contribution on a 75,000 salary yields a personal contribution of 4,500 per year.

- Employer Matching Structure

Most employers offer a matching contribution, which is essentially free money that helps your account grow faster. The calculator handles two primary matching models:

- Dollar-for-Dollar Match (100%): The employer matches 100% of your contributions up to a specific limit (e.g., 3% of your salary).

- Partial Match (e.g., 50%): The employer matches half of what you put in, up to a set cap (e.g., matching 50% of your contributions up to 6% of your salary).

- Economic Assumptions

- Expected Annual Return: The average rate of growth you expect from your underlying investments (historically, a diversified equity portfolio averages 7% to 10% before inflation adjustments).

- Annual Inflation Rate: Helps you see what your future balance is actually worth in today’s dollars by adjusting the projected total for future purchasing power.

Key Financial Projections You Will Receive

- Projected Retirement Balance: Your total estimated nest egg at your targeted retirement age, reflecting personal contributions, employer matching, and compounding returns.

- Cumulative Personal Contributions: The total out-of-pocket sum you contributed throughout your career.

- Total Employer Match: The lifetime monetary sum contributed by your employer.

- Upfront Income Tax Savings: Traditional 401(k) contributions are made with pre-tax dollars, lowering your current taxable income. The calculator estimates these annual tax savings based on your marginal income tax bracket.

Professional Strategies to Optimize Your 401(k) Performance

Secure the Full Employer Match

If your employer offers a match, contribute at least enough to capture the entire match. For example, if your employer matches up to 6% of your salary, setting your personal contribution rate to anything lower than 6% means leaving free compensation on the table.

Use the “Plus-1%” Annual Strategy

If you cannot afford to contribute the legal maximum immediately, start with a comfortable rate and increase your contribution by 1% each year. Aligning this 1% increase with your annual raise makes the adjustment easier to manage.

Be Mindful of Expense Ratios

While your employer chooses your 401(k) provider, you choose the underlying investments. Look for low-cost index funds with low expense ratios (ideally under 0.20%). High management fees can chip away at your compounding returns over several decades.

Catch-Up Contributions (Ages 50+)

If you are 50 or older, take advantage of IRS catch-up provisions. These rules allow you to contribute extra funds beyond the standard annual contribution limit, helping you build your savings as you near retirement.

Frequently Asked Questions (FAQ)

What is a good return rate to assume for a 401(k) projection?

For long-term planning, assuming an annual return of 6% to 8% is a conservative, realistic baseline. While the historical long-term average of the stock market is closer to 10%, factoring in inflation or opting for a more conservative asset mix as you age makes a lower estimate safer for retirement projections.

What is the difference between a Traditional 401(k) and a Roth 401(k)?

The main difference is when your contributions are taxed:

- Traditional 401(k): Funded with pre-tax dollars, which lowers your current income tax. Withdrawals in retirement are taxed as ordinary income.

- Roth 401(k): Funded with after-tax dollars, meaning you get no upfront tax break. However, all qualified withdrawals in retirement are completely tax-free.

When am I fully owned of my employer’s matching contributions?

This depends on your company’s vesting schedule. While your personal contributions are always 100% yours, employer matching funds often vest over time (e.g., a 3-year cliff or a 5-year graded schedule). Be sure to check your company’s plan details to see when those matched funds are officially yours to keep if you leave the company.

To examine other core calculations, numeric conversion models, or system metric parameters, navigate through our comprehensive computational directories at /number-conversion/.